{kind=link}

As far as headlines go, the banking sector has emerged because the undisputed champion of the March quarter (This autumn) earnings season thus far.

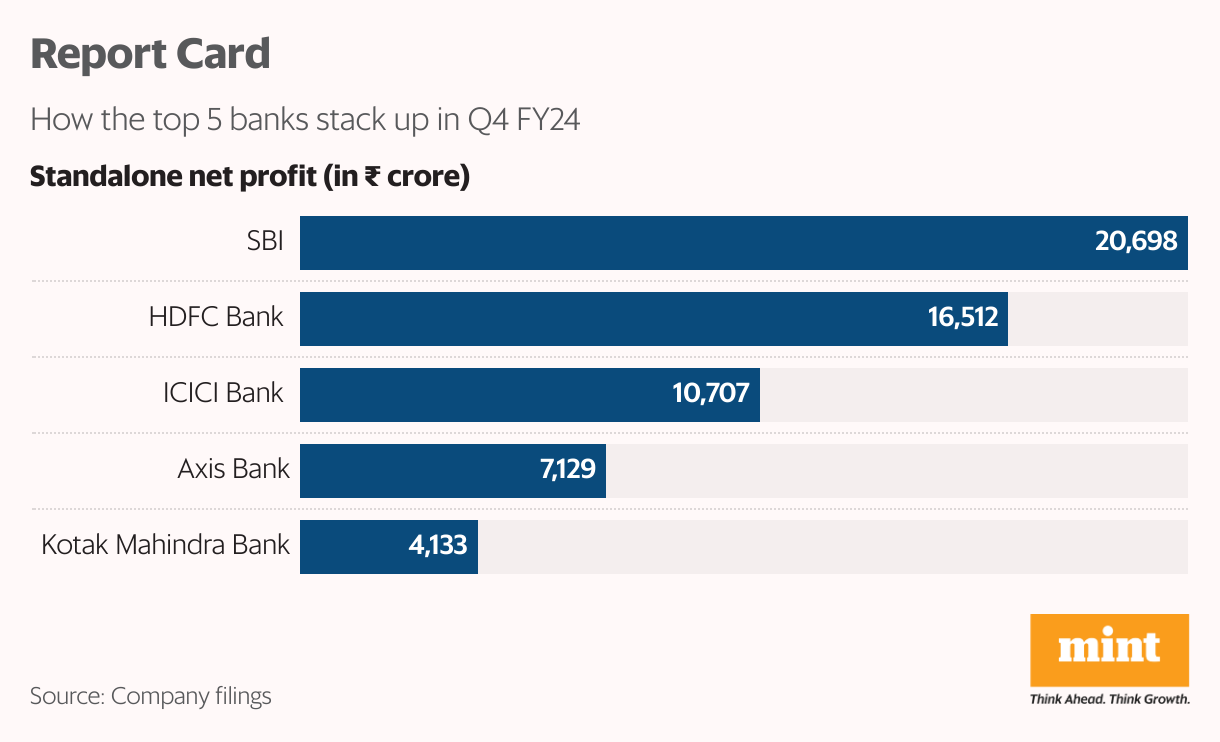

The nation’s largest lender, State Bank of India (SBI), posted a internet revenue of ₹20,698 crore in This autumn, which isn’t solely its highest-ever determine but in addition the largest quarterly revenue by any Indian financial institution. SBI additionally pipped India’s most respected firm Reliance Industries, which had logged a internet revenue of ₹18,951 crore within the quarter.

Another state-run lender which delighted traders was Punjab National Bank, whose internet revenue soared nearly three-fold to ₹3,010 crore, propelled by a soar in curiosity earnings and declining bitter loans.

All the non-public sector biggies, too, are firing on all cylinders, with revenue progress of almost 20% amid wholesome disbursals.

Retail romp

View Full Image

One of probably the most conspicuous elements underpinning banks’ efficiency within the final quarter of 2023-24 was regular mortgage progress, within the vary of 15-25%. The progress was primarily led by the high-yielding retail section, with the company vertical staying flat and even posting a decline in some circumstances.

HDFC Bank, the nation’s largest non-public sector lender, noticed a 3.5% sequential uptick in retail loans, whilst the company and wholesale ebook shrunk 2.2%. Both numbers have been larger than the corresponding interval in 2022-23, however year-on-year figures will not be comparable because the financial institution concluded its mega merger with HDFC on 1 July 2023. The retail vertical contains 50.6% of its mortgage ebook, adopted by industrial and rural banking (CRB) at 32.3% and company and wholesale at 17.1%.

ICICI Bank, too, noticed retail loans rising at a wholesome clip of 19.4% on-year, pushed by mortgages (up 14.9%), private loans (up 32.5%) and bank cards (up 35.6%). Retail accounts for 54.9% of its whole loans, whereas for Axis Bank, it’s even larger at 60%. Despite the upper base, Axis Bank noticed its retail advances develop 19.6% year-on-year, in comparison with small and medium enterprises (SME) at 17.7% and company at simply 3.3%.

“Within retail, administration continues to give attention to high-yield segments like rural loans (+15% quarter-on-quarter or q-o-q), private loans (+10% q-o-q), small enterprise banking (+6.9% q-o-q) and bank cards (3.4% q-o-q). It clearly acknowledged its intention to develop segments with excessive risk-adjusted return on capital,” analysts at BNP Paribas stated in a note.

Another heartening pattern was the persevering with enchancment in asset high quality. Both non-performing loans and slippages have been at steady ranges for lenders.

“Credit progress continues to be sturdy for many of the banks; there was a pickup in yields in numerous merchandise, which has helped defend internet curiosity margins (NIMs). Asset high quality continues to be benign throughout product portfolios and among the banks are utilizing the present surroundings to make contingency or floating provisions, which is a step in the fitting course,” Christy Mathai, fund supervisor—fairness at Quantum Asset Management Company, instructed Mint.

Credit progress continues to be sturdy for many of the banks; there was a pickup in yields.

—Christy Mathai

Rock and arduous place

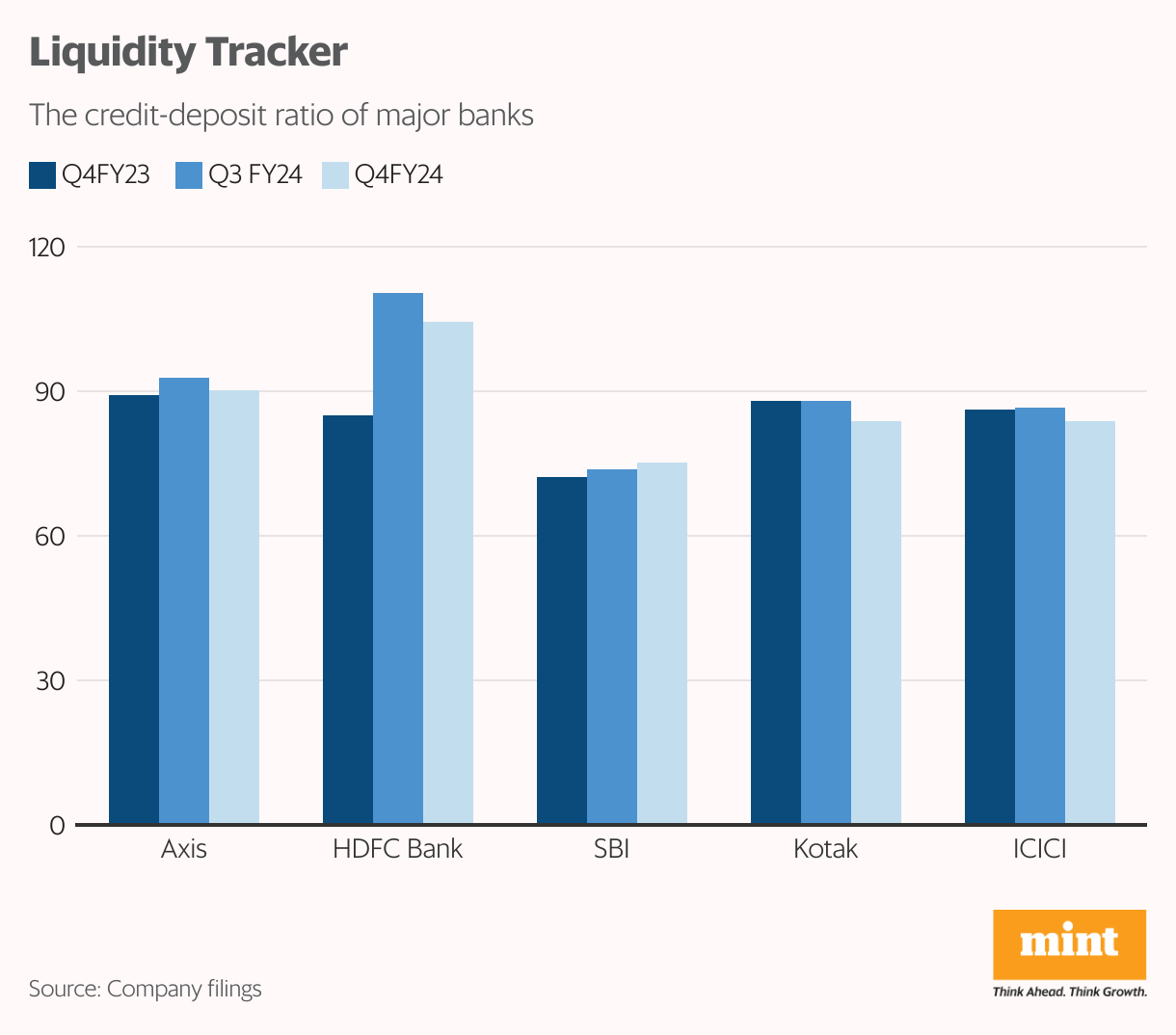

The strong, post-pandemic financial restoration has seen a surge in credit score progress, particularly within the retail section. However, this has additionally led to banks’ loan-to-deposit ratio (LTD) ratcheting up as deposit progress has did not preserve tempo.

The credit-to-deposit (CD) ratio or LTD is a key liquidity gauge of a financial institution which exhibits how a lot of its deposits have been given out as loans. For instance, a CD ratio of 80% means a financial institution has lent out ₹80 of each ₹100 raised as deposits.

A excessive CD ratio, subsequently, poses liquidity and credit score dangers for a financial institution. If a excessive portion of a financial institution’s deposits is lent out as loans, then any unexpected spike in withdrawals can pose an existential menace for the lender.

The CD ratio of banks is at a decadal excessive of 80%, CareEdge Ratings acknowledged in a March 2024 report.

While there isn’t a regulatory threshold which has been prescribed for the CD ratio, a vary of 70-80% is usually seen as wholesome. In December final yr, the Reserve Bank of India (RBI), India’s central financial institution, had reportedly requested some lenders with high CD ratios to bring the number under control.

This is the place lenders face Sophie’s selection.

There are solely two methods to deliver down a ratio— both lower the numerator or improve the denominator. Decreasing the numerator (that is credit score) means sacrificing progress, which any firm is loath to do. The different choice, rising the denominator (deposits), would dent margins as banks would want to pay larger curiosity to draw depositors. Hard as it’s, the second is the one viable choice. But like most issues in life, it’s simpler stated than carried out.

Credit progress has outstripped deposit progress for the previous few monetary years. In 2023-24, in opposition to a deposit progress of 13.5%, credit score progress stood at round 20%. The credit score progress determine has additionally acquired a enhance following the mega merger of HDFC and HDFC Bank, however even adjusting for that, the quantity stands at about 16%.

According to RBI information, financial institution credit score progress exceeded the deposits improve by ₹2 trillion in 2023-24. A key contributor to this pattern has been the rise of equities as an asset class.

Credit progress has outstripped deposit progress for the previous few monetary years. In 2023-24, in opposition to a deposit progress of 13.5%, credit score progress stood at round 20%.

Retail traders have made a beeline to Dalal Street amid this multi-year bull run.

From 40 million on the finish of 2019-20, the variety of demat accounts has vaulted to 151 million as of March 2024. Monthly inflows into mutual funds by way of systematic funding plans (SIPs) have additionally marched larger, crossing the ₹20,000 crore-level for the primary time in April. Assets beneath administration (AUM) of the home mutual fund business breached the historic mark of ₹50 trillion in December 2023, almost doubling from ₹25.5 trillion within the quarter ended June 2020.

Mutual fund AUMs stand at ₹57.3 trillion at current. Though that is nonetheless round a fourth of whole financial institution deposits (greater than ₹200 trillion), the incremental fund flows are skewed extra in direction of equities (and different asset courses like gold and actual property) slightly than the ‘old-fashioned’ and tax-inefficient financial institution mounted deposits.

While the highest lenders posted encouraging deposit progress in This autumn (HDFC Bank at 7.5% q-o-q; Axis Bank at 6.3%; ICIC Bank at 6%), the share of present account and financial savings account (CASA) deposits—the most affordable supply of funds for banks—lagged on an annual foundation.

Bank managements are aware of the problem at hand.

“The key focus over the medium to long run (medium is between two and three years) is to give attention to bettering our profitability metrics outlined because the ROAs (return on property) and the earnings per share. To obtain that, the secret is to make sure the sustainability of our deposits franchise, particularly the retail deposits franchise,” Sashidhar Jagdishan, HDFC Bank’s managing director and chief executive officer, stated throughout its post-earnings name.

View Full Image

Jagdishan acknowledged that there may be a “aggressive surroundings” in the retail deposit market but added that the company will not overpay for funds but rather bank on its “enhanced customer engagements and elevated service-first culture”.

But will depositors be glad with “enhanced buyer engagements” at the price of larger returns?

Most new traders anyway desire equities over debt, whereas even for financial institution mounted deposit holders, the combination motion is in direction of searching for larger yields.

As per the most recent quarterly information from RBI, rising return on time period deposits has been driving the compositional shift in financial institution deposits. The share of time period deposits in whole deposits elevated to 60.3% in December 2023 from 57.2% in March 2023.

On an incremental foundation, time period deposits accounted for almost 98% of the whole deposits with scheduled industrial banks throughout April-December 2023, whereas the share of CASA deposits went down.

Not simply that, deposits moved to larger rate of interest buckets—the share of time period deposits bearing over 7% rate of interest rose to 61.4% of the whole time period deposits in December 2023 from 54.7% a quarter in the past and 33.7% within the year-ago interval.

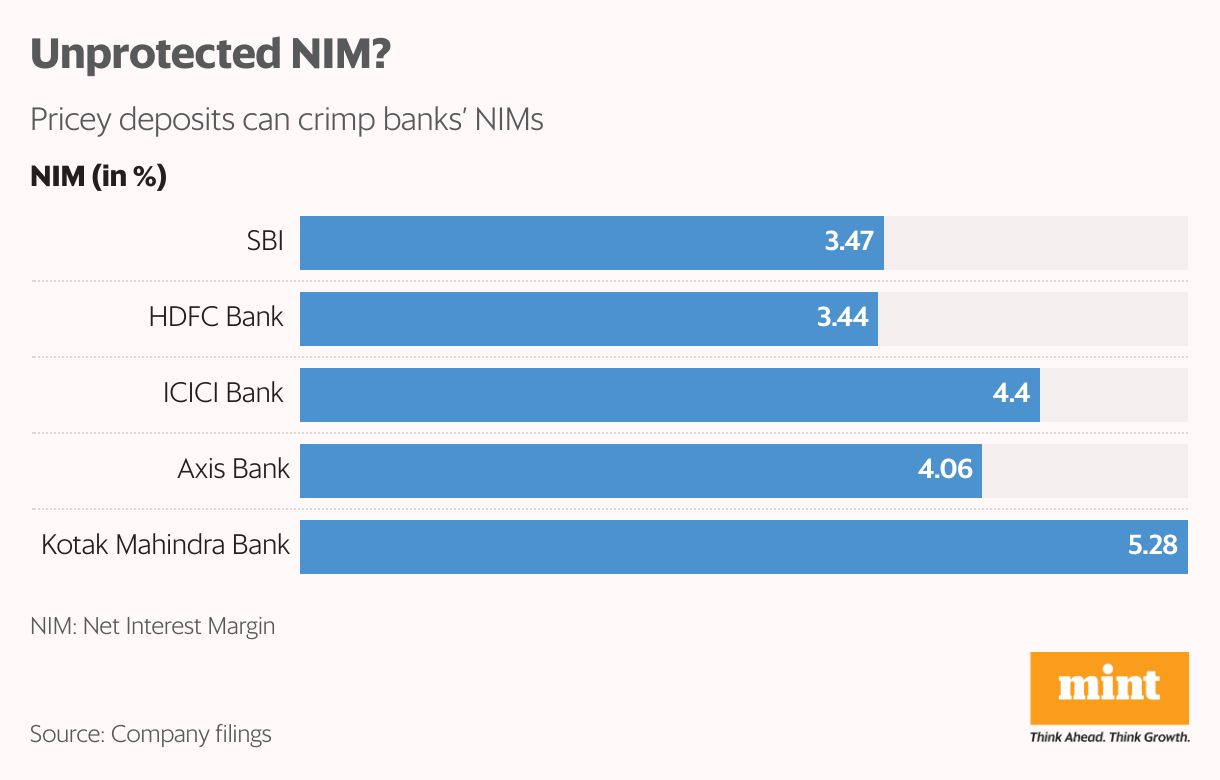

Against this backdrop, most analysts count on banks’ funding value to inch larger as they compete for deposits, which can consequently weigh on their internet curiosity margins (NIMs) or the distinction between the curiosity earnings earned and the curiosity paid by a financial institution.

The spike in value of funds (CoF) was clear within the This autumn earnings. HDFC Bank’s CoF rose to five.66% from 4.32% within the year-ago quarter, whereas that of ICICI Bank was at 5% (from 4.2%) and Axis Bank at 5.2% (from 4.5%).

Revising its outlook on the home banking sector from constructive to destructive final month, rankings company Icra stated banks’ tempo of progress is predicted to reasonable in 2024-25 amid challenges in deposit mobilization and regulatory tightening. With the share of CASA in whole deposits persevering with to say no, it stated dear deposits will crimp banks’ NIMs this monetary yr.

SBI, which had a blockbuster quarter, noticed its internet curiosity earnings rise by simply 3% year-on-year, exhibiting the burden of upper value of deposits.

However, some specialists additionally preserve that the hit on margins won’t be as excessive as many concern.

“There are two elements. One, liquidity was tight within the system on account of the federal government not spending sufficient, and that ought to reverse publish the elections,” Kaitav Shah, lead BFSI analyst at Anand Rathi Institutional Equities, told Mint. “Secondly, in Q4, both CASA and term deposits have shown strong growth, although that might not be replicable in Q1 FY25 for most of the banks. The credit-deposit ratio could again inch up a bit, which will protect the NIMs, but we don’t expect a sharp hike in deposit rates,” he added.

Tech speak

When software program is consuming the world, can banking be far behind?

One notable pattern on this earnings season was the elevated give attention to banks’ know-how arsenal. Managements additionally spent a good bit of time detailing their IT spends and digital choices in the course of the post-earnings calls. So a lot so, some analysts even singled out digital capabilities as one of many key differentiators for assessing banks.

Vocalizing a difficulty common with a part of netizens, BNP Paribas famous how clients’ disappointment with HDFC Bank’s app is a matter of concern. “The app is, in some ways, the face of its know-how technique and successfully its department presence within the new digital world. Two delays on app revision timelines doesn’t bode effectively, in our view,” it acknowledged.

“Structural considerations with legacy information structure are one thing HDFC Bank shares with different older banks. Given their efficiency on the entrance finish (app), efforts to repair the deeper, extra structural drawback come beneath a cloud for certain, in our opinion. This will turn out to be incrementally related to our thesis as the primary leg of valuation re-rating from at the moment distressed ranges is accomplished,” it added.

In distinction, it applauded ICICI Bank’s tech structure.

“The financial institution’s tech and digital funding efforts seem to have set the benchmark amongst giant private-bank friends. While the iMobile app’s reputation gives us some proof of the financial institution’s tech and digital focus, its efforts span segments and features,” it stated in one other report.

Analysts at home brokerage agency Geojit highlighted how ICICI Bank’s digital transformation permits it to increase its distribution. “Strong progress momentum in advances and deposits is predicted to proceed, because the financial institution with its technological development and higher attain is well-equipped to capitalize on rising demand,” they stated.

Road forward

The ‘war for deposits’ just isn’t solely posing a menace to banks’ margins however to credit score progress itself.

S&P Global Ratings expects the sector’s credit score progress to reasonable to 14% this yr from 16% in 2023-24 if deposit progress stays tepid. “We count on banks to deliver down their mortgage progress in FY25 and produce it consistent with deposit progress. If banks don’t do that, they might be paying larger to get wholesale funding, which can affect profitability,” Nikita Anand, S&P Global Ratings director, South and South-east Asia, stated throughout a webinar on 24 April.

That stated, analysts preserve that because the underlying fundamentals of the financial system stay sturdy, the present predicament of banks is a momentary and never a structural problem.

“Over a longer interval, at a system stage, credit score progress drives deposit creation within the financial system. So, we don’t count on the present state of affairs to persist over the long term,” Quantum’s Mathai stated.