The backside 80% firms accounted for 0.3% share in complete earnings of the BSE-listed universe in 2023-24, the highest in seven years, a Mint evaluation of knowledge for 4,006 firms confirmed. The determine had recently been languishing beneath zero, on account of the dominance of loss-making firms. The share of loss-makers in the pattern is down at 24% from practically 33% in 2019-20 and 26% in 2021-22.

The prime 10% firms nonetheless command a 95% revenue share, but that’s down from 97% in 2021-22. Their share had peaked at an uncommon 127% in 2019-20, when many firms reported losses amid already falling world demand and commodity costs, with added stress on account of the seven days of covid-19 lockdown. (It’s doable for a set of firms to have greater than 100% revenue share on account of the presence of loss-making firms.) The evaluation categorized firms into deciles based mostly on their newest income, i.e., the greatest 10% revenue-earners, the subsequent 10%, and so forth.

The developments mirror broader trade dynamics. “The variations seen in efficiency can be extra on account of particular trade traits,” said Madan Sabnavis, chief economist at Bank of Baroda. “For example, the years in which crude oil prices are high and oil marketing companies hold on to their prices, their profits would take a hit and vice versa.”

Despite a loosened grip on earnings, bigger firms appear poised to keep up their outsized share given their deep pockets and model energy, consultants imagine. Modest declines in revenue focus are doubtless as market dynamics evolve and smaller firms adapt.

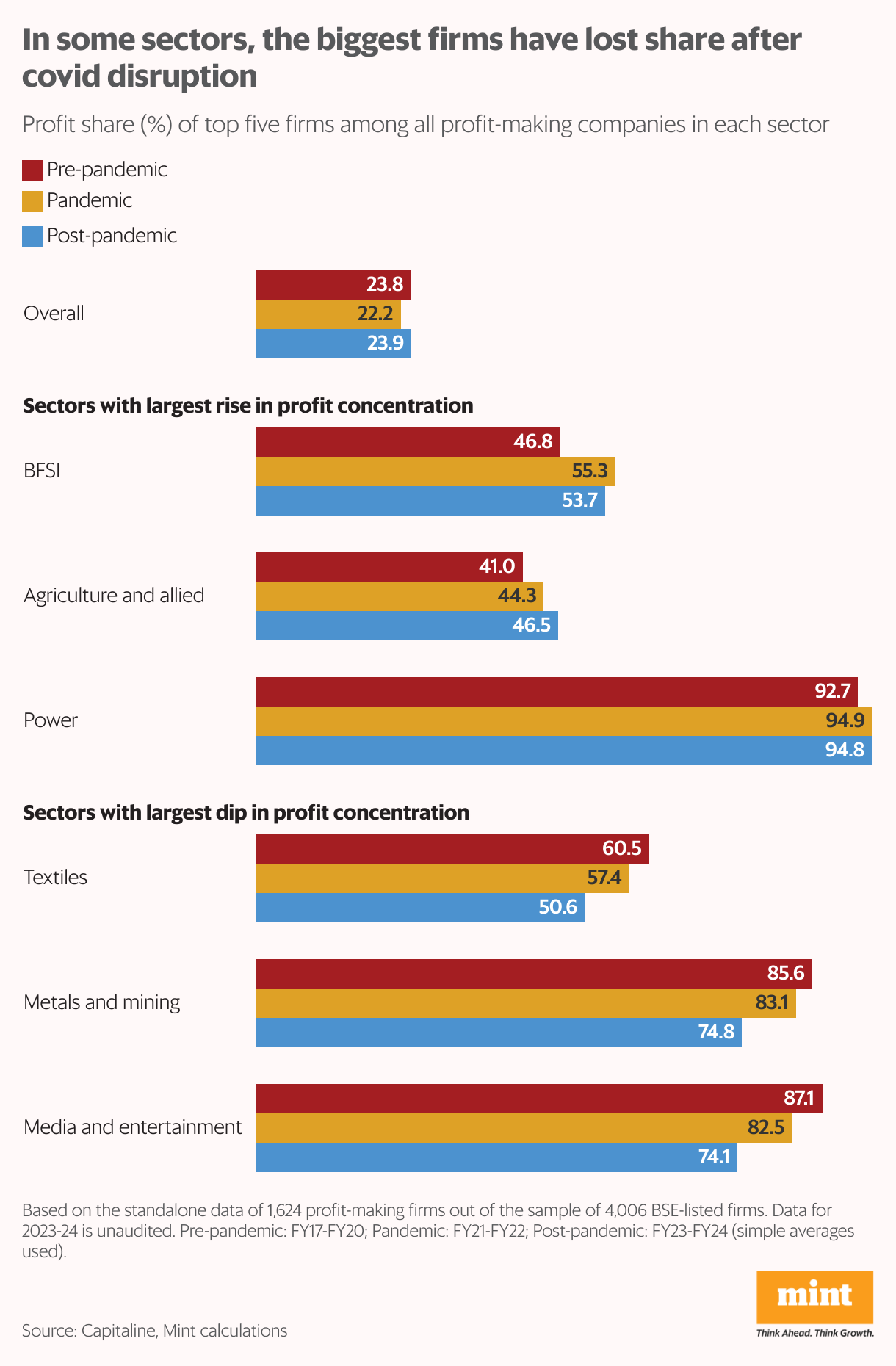

In 13 out of 17 sectors, the prime 10 firms have seen a post-pandemic dip in revenue focus, most prominently in media, metals and mining, and textiles. “Consumers’ choice for on-demand and customized content material has reshaped media and leisure, whereas smaller gamers in textiles are benefiting from provide chain resilience,” said Sujan Hajra, chief economist and executive director, Anand Rathi Shares and Stock Brokers.

Also learn: Echoes of oligopoly as big firms get bigger

Banking growth

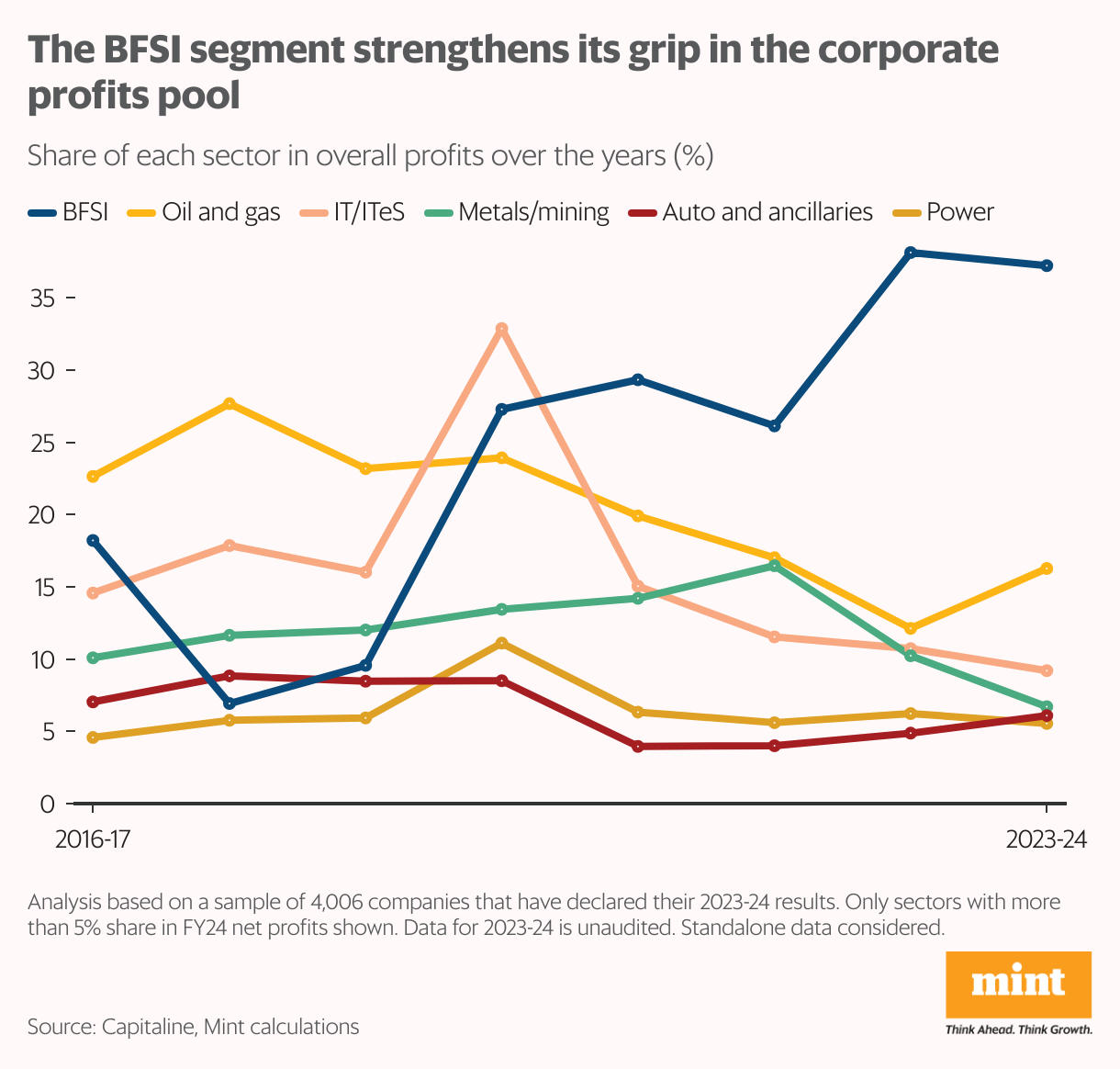

Over half of India Inc.’s web earnings in 2023-24 got here from the banking, monetary providers, and insurance coverage firms (BFSI) and oil and fuel sector, taking their revenue focus to at the least an eight-year excessive. However, whereas BFSI’s revenue share has surged quickly—from 18.2% seven years in the past to almost 37% now, that of the oil and fuel sector (which operates beneath a stringent regulatory regime) dipped from 23% to almost 16% in the similar interval.

“The monetary sector’s dominance in India is rooted in complete reforms and liberalization, which, regardless of preliminary hardships, have strengthened the sector,” Hajra famous. The BFSI section’s revenue edge is prone to persist in a rising economic system, fuelled by excessive credit score demand.

Also learn: The pockets of stress in India Inc’s improving credit health

The different two profit-making powerhouses—data expertise (IT), which is reeling beneath a slowdown, and metals and mining, whose revenue realizations are down on account of decrease commodity costs—have witnessed gradual declines in their revenue share to beneath 10%.

Top weapons’ clout

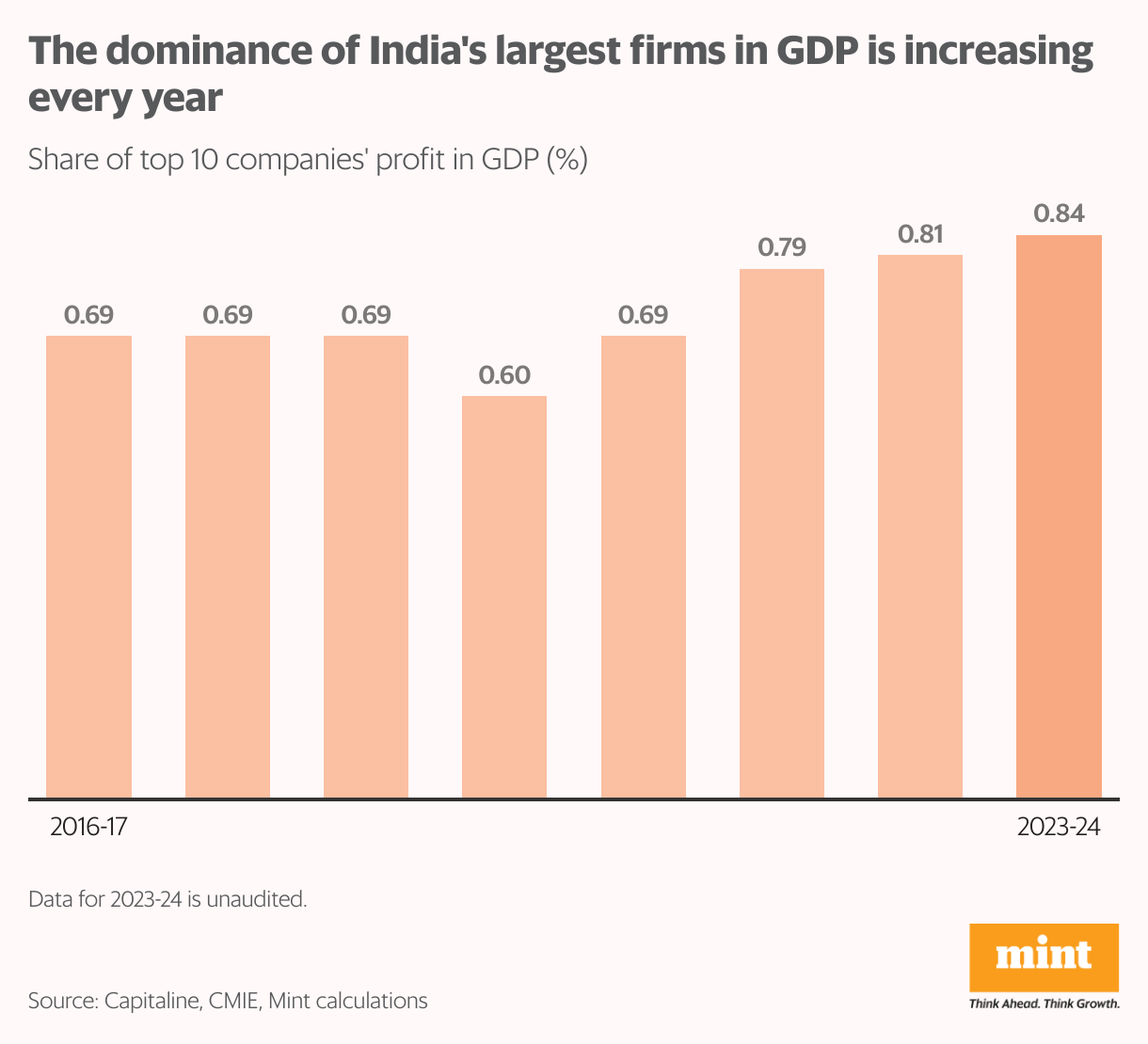

The declining revenue focus amongst the biggies is not to say their clout is declining. The earnings of the prime 10 firms in the pattern made up 0.84% of India’s general financial output in 2023-24, steadily rising from 0.69% seven years in the past to the highest on this interval. The mixture earnings of the full pattern as a share of gross home product have additionally risen to an eight-year excessive to 4%.

This once more illuminates a troubling development of earnings being concentrated amongst only a handful of sectors. Financial providers, oil and fuel, and IT proceed to reign supreme at the prime of the pyramid, and their constant dominance is a testomony to sustained market management. Experts argue that whereas earnings may fluctuate in the coming years, these sectors will proceed to keep up huge gross sales volumes, doubtless resulting in elevated focus. However, it raises questions on broader market dynamics and revenue distribution in the wider company panorama.

Demand outlook

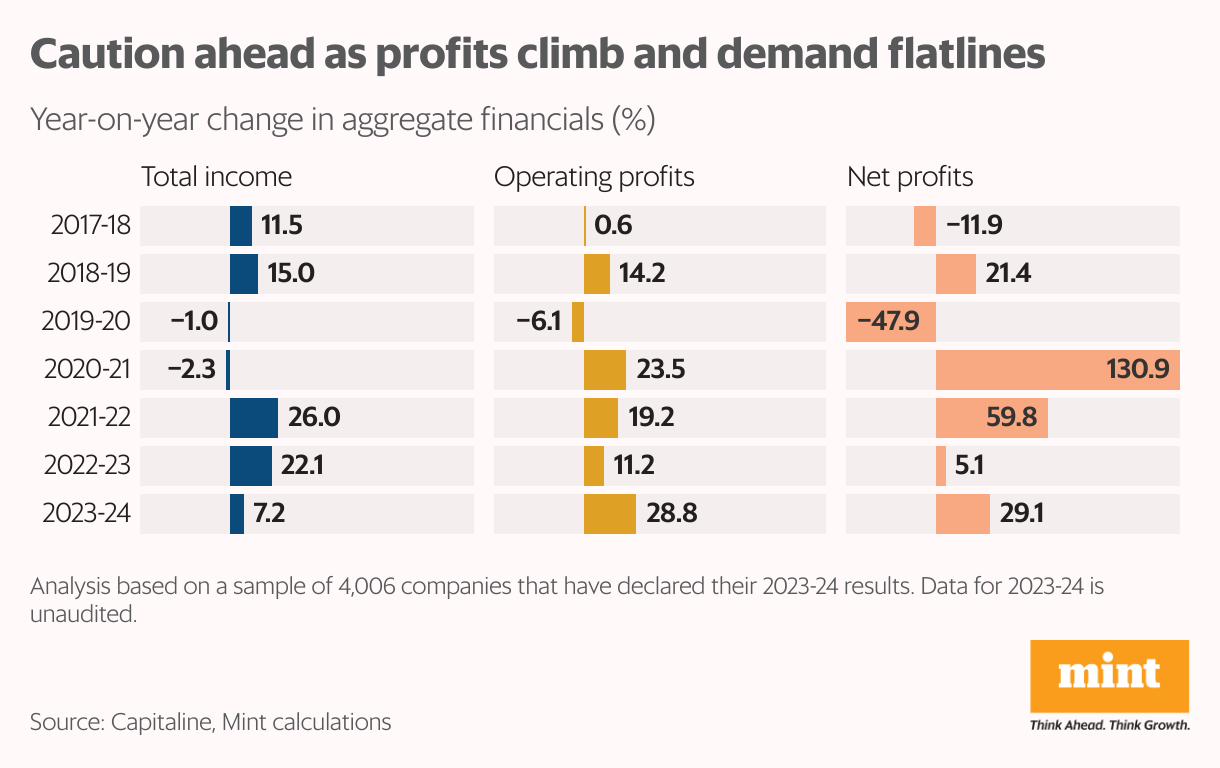

After the pandemic, leaner operations and easing commodity prices led to a windfall for company earnings, serving to the web revenue margins of the pattern shoot up by practically 2.4 share factors (from 7.6% of income to 10%)in the last 4 years. But a cost-cutting knife isn’t sustainable. “Continuous funding in innovation and expertise is essential for enduring profitability,” Hajra said.

In 2023-24, the mixture earnings of the pattern surged 29%, but it could possibly be difficult to keep up the momentum. “There can be moderation in revenue development for positive on account of base results,” stated Sabnavis. Demand has been sketchy (mixture gross sales grew simply 7%), although Sabnavis stated it was prone to get better this 12 months, and could be extra seen after the harvest season in October when the pageant season can be at its peak.

This is the first a part of a three-part information journalism collection that includes a company well being check-up in the post-pandemic interval.

Also learn: The two faces of India Inc.’s Q3 growth story

{kind=link}