{kind=link}

What these lengthy photographs don’t present is all of the particles that the ocean throws again day-after-day. Once one sees the seashore suffering from particles—which the native municipality is both torpid about cleansing up or maybe struggling to—one realizes that the setting is not as stunning as soon as the image is full.

The Indian economic system is a tad like that. In 2023-24, the scale of the economic system or its gross home product (GDP) grew 8.2% in actual phrases adjusted for inflation, an excellent growth determine. Nonetheless, the non-public consumption expenditure, the cash you and I spend on shopping for issues and the biggest a part of the economic system—which over time has fashioned round 55-60% of its measurement—grew by simply 4%, the slowest since 2002-03, ignoring the pandemic yr of 2020-21. In nominal phrases, not adjusted for inflation in 2023-24, non-public consumption grew 8.5%, the slowest since 2004-05, ignoring 2020-21.

At the identical time, in 2023-24, the growth in retail lending by banks was at its highest ever degree, since information first grew to become out there in 2008-09. Retail lending by banks includes housing loans, automobile loans, training loans, credit card outstandings, private loans, loans given in opposition to fastened deposits, shares, bonds, gold jewelry and many others. Typically, one would assume that retail lending growth and personal consumption growth would have a robust correlation.

In 2023-24, retail lending of banks grew 27.5% and personal consumption grew 8.5%, the previous at its quickest tempo ever and the latter virtually at its slowest tempo in 20 years, resulting in a scenario the place the distinction between the 2, was at its highest ever degree (see chart). This distinction has been considerably excessive in three of the final 5 monetary years, compared to the years earlier than that.

So, what is taking place right here? What are the impacts of this dichotomy? We will attempt answering these questions and extra on this piece.

Retail Aggression

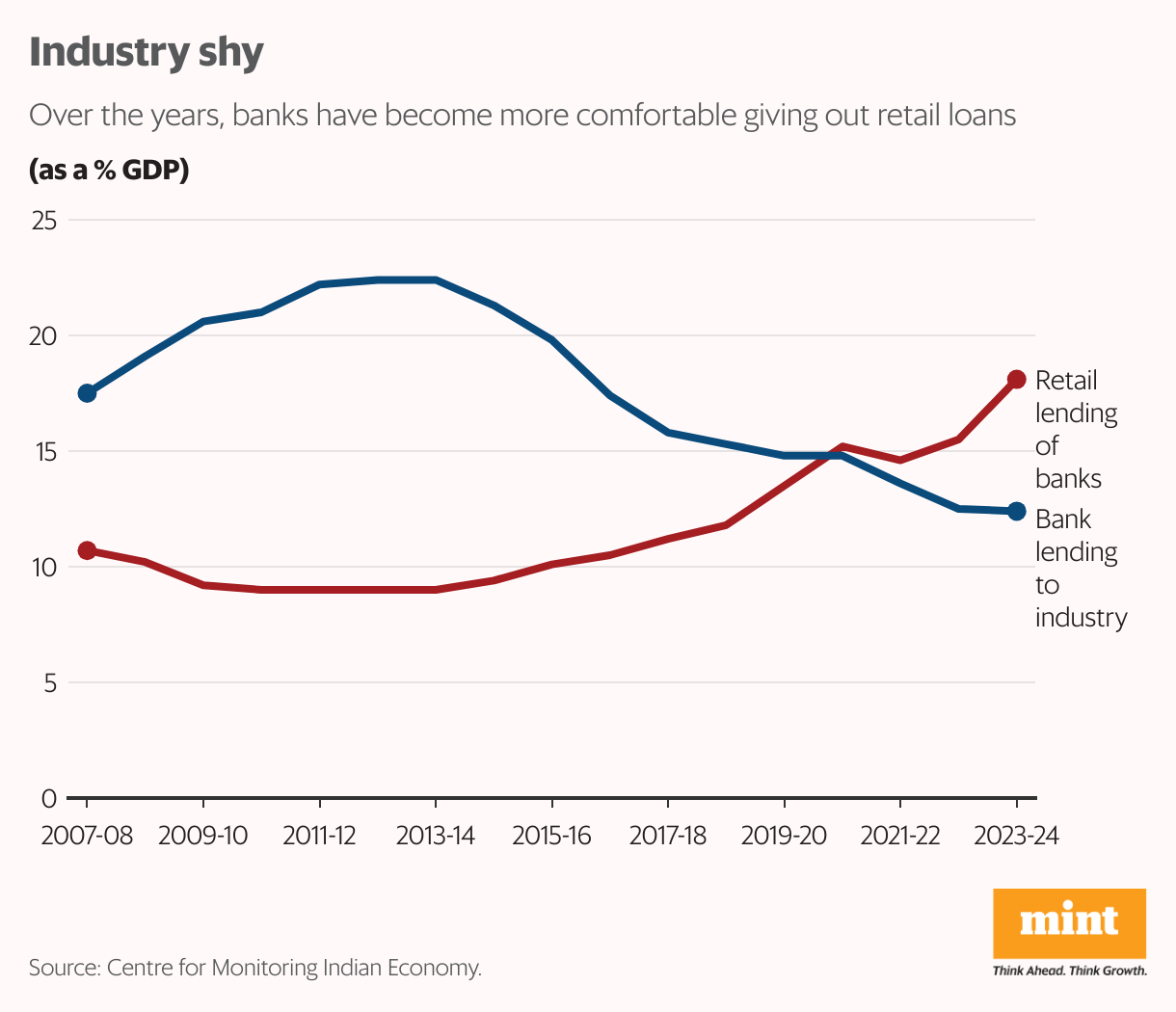

In 2007-08, the financial institution lending to trade stood at 17.5% of the GDP. Their retail lending was at 10.7%. The lending to trade peaked at 22.4% in 2012-13 and has been falling since. In 2023-24, it stood at 12.4%, the bottom since such information grew to become out there from 2007-08 onwards. In truth, retail lending by banks first overtook their lending to the trade in 2020-21. In 2023-24, it stood at 18.1% of the GDP, the very best degree ever (see chart).

Essentially, over time, banks have turn out to be extra snug carrying out retail lending.

This is an affect of the dangerous loans drawback they needed to face within the 2010s totally on account of company mortgage defaults. Also, company funding growth continues to stay on the slower aspect, limiting lending alternatives.

Further, the general retail lending of banks is larger than 18.1% of the GDP as a result of banks additionally lend to non-banking finance firms (NBFCs), which perform retail lending. In 2023-24, the financial institution lending to NBFCs stood at 5.2% of the GDP, the very best ever.

In truth, there is some cause to fret on this entrance. As the Reserve Bank of India’s (RBI’s) newest Financial Stability Report (FSR) said: “In the buyer credit phase, there are a couple of considerations…First, delinquency ranges amongst debtors with (retail loans) beneath ₹50,000 stay excessive. In specific, NBFC-fintech lenders, which have the very best share in sanctioned and excellent quantities, even have the second highest delinquency ranges, solely beneath that of small finance banks.”

View Full Image

Indeed, the sharp growth in financial institution lending to NBFCs from 2.5% of the GDP in 2016-17 to five.2% in 2023-24, suggests the rise of fintech’s lending cash. Also, with loans simply out there over a smartphone, there was a drop in lending requirements on the decrease finish of the market, resulting in larger delinquencies.

The Structure

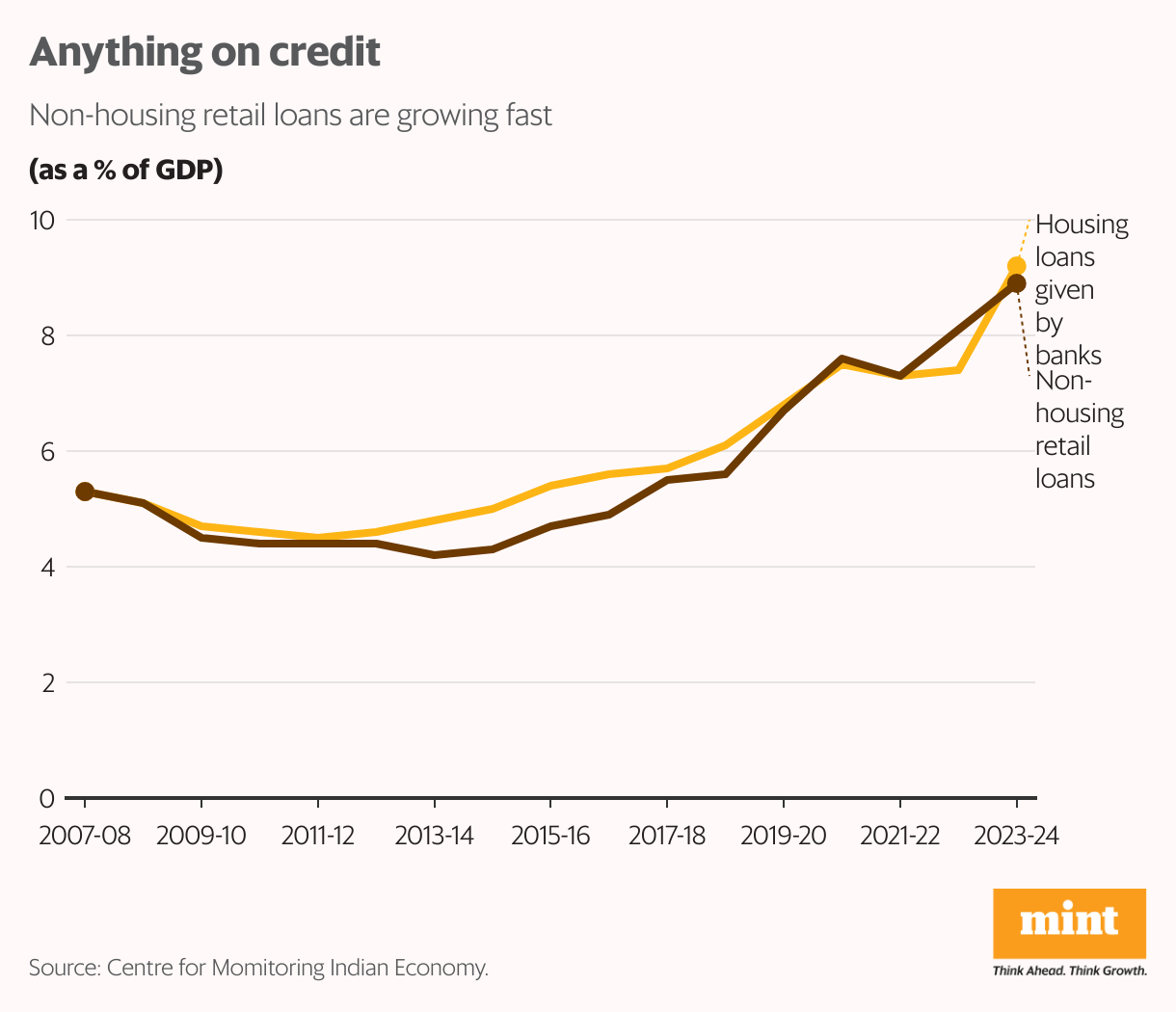

When it involves retail loans, the division between housing loans and non-housing loans is round half and half. In the final 5 years, from the top of 2018-19 to the top of 2023-24, non-housing retail loans have grown by 19.7% per yr on common. In comparability, housing loans have grown by round 18.6% per yr on common. But this comes with a disclaimer. An excellent portion of housing mortgage growth got here between the top of 2022-23 and the top of 2023-24, once they grew 36.7%. If we have a look at the four-year interval between 2018-19 and 2022-23, they’ve grown at a a lot slower tempo of 14.5% per yr on common.

So, what does the quick growth in non-housing retail loans inform us? As a January 2024 information report within the Business Standard identified: “The common promoting value [of a car] has gone up from ₹7.65 lakh in 2018-19 to ₹11.5 lakh in 2023-24, up by over 50%.”

This is as a result of most buyers now want to buy higher end variants and never as a result of cheaper automobiles are now not out there. A December 2022 information report in The Newz9 mentioned: “70% of iPhone purchases in India are on EMIs.” While this information report is greater than a yr outdated, there is no cause to imagine that this case would have modified materially by now.

Indeed, shopping for costly depreciable belongings like automobiles and cellular by taking up a mortgage—as the author Jonathan Raban places it in Soft City in a barely completely different context—is “to boost the identities” of their purchasers. “Their most important function is to tell us something about the people who buy them; they belong to the hazardous but necessary urban art of self-projection,” writes Raban.

We dwell in an period the place persons are perpetually scrolling on their smartphones to observe reels and shorts wherein different persons are attempting to inform the world at massive what a superb time they’re having.

What explains this? We dwell in an period the place persons are perpetually scrolling on their smartphones to observe reels and shorts wherein different persons are attempting to inform the world at massive what a superb time they’re having—with higher telephones, dearer automobiles, extra stunning garments and longer holidays. People watching these reels are needled to affix in, by shopping for dearer automobiles and telephones, on credit. People don’t wish to wait.

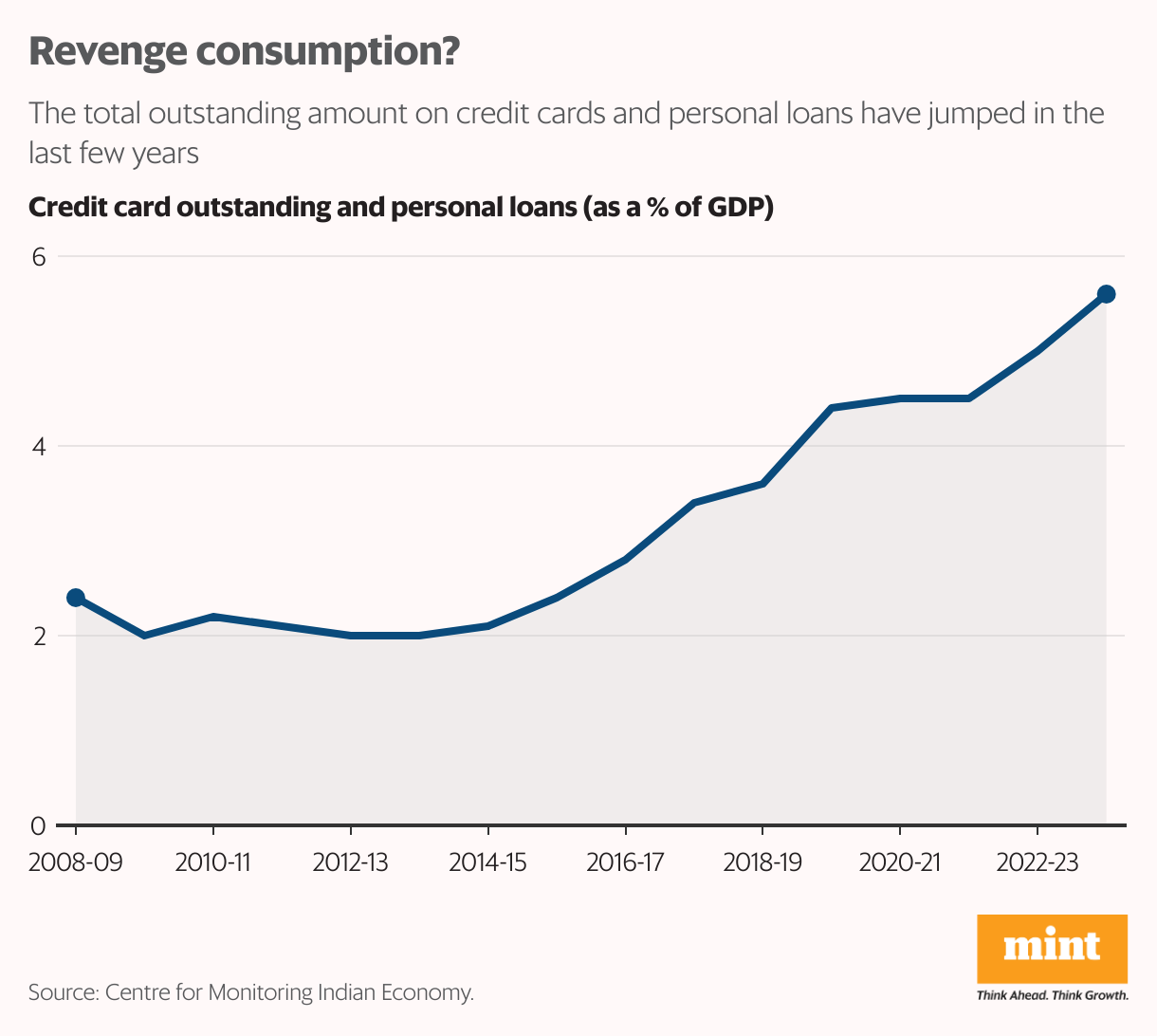

This additionally explains to some extent why the entire excellent quantity on credit playing cards and private loans has jumped from 3.6% of the GDP as of the top of 2018-19 to five.6% as of the top of 2023-24. People are utilizing these modes to spend extra to maintain up with the Sharmas. Some might say this is revenge consumption put up the pandemic.

The RBI is frightened about this quick growth in retail loans. As it factors out within the newest FSR, the classic delinquency of retail loans stays comparatively excessive at 8.2%. Vintage delinquency is outlined as the proportion of accounts which have turn out to be delinquent—that is mortgage reimbursement hasn’t occurred for 90 days or extra—inside twelve months of origination of the mortgage. Of course, this is not an issue on the banking sector degree as a result of the massive retail loans, that is automobile loans and housing loans, aren’t being defaulted on, however smaller ones are.

The Struggle

What does the default of smaller retail loans imply? It primarily implies that a big part of the inhabitants is struggling on the earnings entrance. And these loans are probably getting used to finance day-to-day consumption. Also because the RBI’s newest FSR factors out: “Little greater than a half of the debtors on this phase [retail loans] have three dwell loans on the time of origination and greater than one-third of the debtors have availed greater than three loans within the final six months.”

What does this inform us? First, loans have turn out to be simpler to avail and which is why credit requirements are falling. Second, it’s just about doable that debtors are taking newer loans to pay off older loans, one thing that corporates did within the 2010s. To say this with higher confidence one would want extra detailed information.

In truth, this battle on the earnings entrance is extra clearly seen after we have a look at the general family debt and never simply retail loans. The economists, Nikhil Gupta and Tanisha Ladha, of Motilal Oswal, in a latest analysis observe, write that family debt includes “agricultural debt, housing loans, non-housing [retail] loans and loans taken by small companies”. The RBI estimates that the family debt as of March 2023 stood at 40.1% of the GDP. Gupta and Ladha estimate that family debt stood at 30% of the GDP as of 2018-19 and is more likely to have jumped to an all-time excessive of 40.9% in 2023-24.

Reason to Worry?

Of the entire family debt of round 41% of the GDP, 11% are housing loans given by banks and housing finance firms. The remaining debt is non-housing debt, which because the Motilal Oswal economists level out “is similar to that in Malaysia and Taiwan, and better than within the US, Japan, and China”.

As per RBI’s FSR: “The…family debt in India is comparatively low when in comparison with different rising market economies, however in relation to GDP per capita, it is comparatively excessive.” This increase in household debt, the RBI’s FSR says, “warrants close monitoring from a financial stability perspective”.

View Full Image

Further, as Gupta and Ladha level out, family debt is anticipated at 52% of private disposable earnings in 2023-24, in opposition to 48% in 2022-23, 40% in 2019-20 and 32% in 2012-13.

Moreover, the RBI’s FSR launched in December 2023 identified that India’s family debt service ratio (DSR)—or the proportion of earnings used to repay loans—is “one of many lowest on this planet”. RBI calculations put it at 6.7% of the income on average. At the same time, calculations made by Gupta and Ladha put the DSR at around 11-12% of the income, which as they say “is not only much higher than its counterparts in other major economies, but has also increased gradually over the past many years”.

This distinction primarily comes on account of the truth that the RBI assumes the residual maturity of loans to be round 12.7 years, whereas Gupta and Ladha put it at 5.5 years, given {that a} important chunk of family debt in India is non-housing debt with short-term maturities.

Loads of financial institution lending is financing depreciating belongings, like cell phones and dearer automobiles, or day-to-day consumption, or properties that are purchased as monetary belongings and saved locked.

And this explains a couple of issues. First, a higher proportion of family earnings is going in the direction of repaying loans than previously. And that in flip explains the slowdown in non-public consumption expenditure, regardless of the large growth in retail lending by banks. On the entire, there is merely much less cash proportionally out there to spend.

Second, it additionally explains why family monetary financial savings—given that folks have been utilizing the next proportion of their earnings to repay loans—fell to a 47-year low of 5.3% of the GDP in 2022-23. In 2023-24, it is anticipated to have improved to five.7%, Gupta and Ladha estimate.

Third, a whole lot of financial institution lending is financing depreciating belongings, like cell phones and dearer automobiles, or day-to-day consumption, or properties that are purchased as monetary belongings and saved locked. As a latest information report in The Indian Express said, quoting G. Hari Babu, nationwide president of the National Real Estate Development Council, that greater than 11 million flats have been purchased for funding functions and saved locked.

So, a superb proportion of financial institution lending in India is not financing the acquisition of belongings which is able to generate earnings within the days and years to return. Of course, it’s not the fault of the banks. But that’s the way in which it is.

To conclude, the lengthy photographs can at all times look extra stunning and conceal the considerably extra essential particulars.

Vivek Kaul is the writer of Bad Money.